When a financial product isn't converting, the instinct is to look at the outcome: the loan that didn't get approved, the account that didn't link, the payment that didn't go through. What gets overlooked (almost every time) is the process that led there.

That process is the onboarding flow. And in Canada, getting it right is challenging in ways most companies don't expect, because Open Banking hasn't fully launched yet.

We covered this in depth in our May 2026 webinar. Watch the recording to see the full session, including the live scoring exercise and Q&A with our client success and open banking teams. Watch the recording →

The problem isn't the product. It's what came before it.

In my five years at Flinks — starting as a technical account manager and now leading client success — I've been part of integrating Flinks into more than 300 onboarding experiences across lending, banking, and fintech. The pattern is consistent: companies optimize for outcomes and neglect the journey that produces them.

The onboarding flow is nothing but a first impression. If it isn't great, chances are you're not going to get the results you're looking for.

Every user who drops off mid-flow is a customer that never converted. A drop-off at the bank-connection step has a direct acquisition cost — it shows up in conversion rate, in funded loan volume, in activated accounts.

Here's what that looks like in practice.

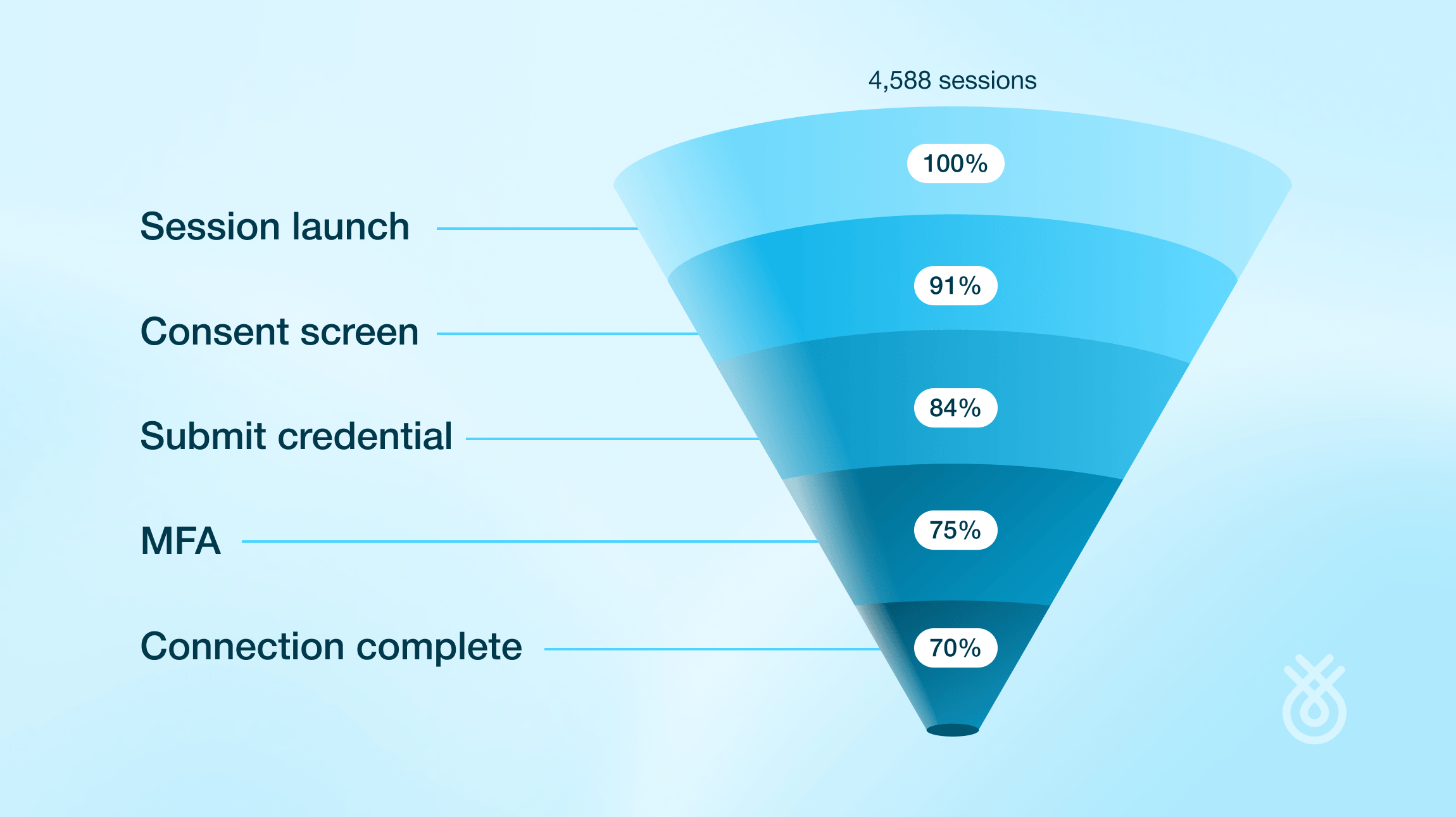

Across a sample of 4,568 onboarding sessions on the Flinks platform, only 70% of users who initiated a bank connection completed it. The drop-off isn't concentrated at one step — it’s distributed across every stage: session launch, consent screen, credential submission, MFA, connection complete. Each step loses a share of the people who made it through the last one.

Across those 300+ integrations, four culprits account for most of that attrition.

The four culprits

Manual steps

Asking users to calculate their monthly income, look up an account number, or manually fill in data that already exists elsewhere is, as my colleague Arber Ago, Enterprise Relationship Manager at Flinks, put it, "like self-checkout at a grocery store, I'm here to spend money at your store, and you're asking me to also check out all the groceries." If a bank connectivity partner is already supplying name, address, income, and account data, that information should be pre-populated for review, not re-entered from scratch.

No flexibility

A single path through onboarding — connect your bank account, or nothing — creates a hard wall for the portion of users who aren't comfortable with that step. In Canada, that portion is meaningful. Open banking hasn't matured here the way it has in the US, UK or Australia. Canadian consumers are increasingly familiar with connecting bank accounts, but they're not universally there yet. Onboarding flows that offer only one path are leaving that segment behind.

Data trust gaps

Users need to know why they're sharing data, what it will be used for, and what controls they have over it. This is basic, but it's frequently absent or buried in legal language. An AI era makes it more acute, not less: fraud has become sophisticated enough that users are right to be skeptical. Take this number from our platform data as an example: an unbranded or unclear consent screen can cost up to 5x more drop-offs than a well-designed one. Transparency and brand consistency in the flow (making the experience feel like it belongs to your product, not a third-party handoff) drives materially higher completion rates.

Connectivity gaps

A great onboarding flow built on unreliable bank connectivity will still fail. The vendor matters. Connection rates across Canadian financial institutions vary significantly depending on the provider, and a drop in connection quality at a critical step is indistinguishable from bad UX from the user's perspective — they just leave.

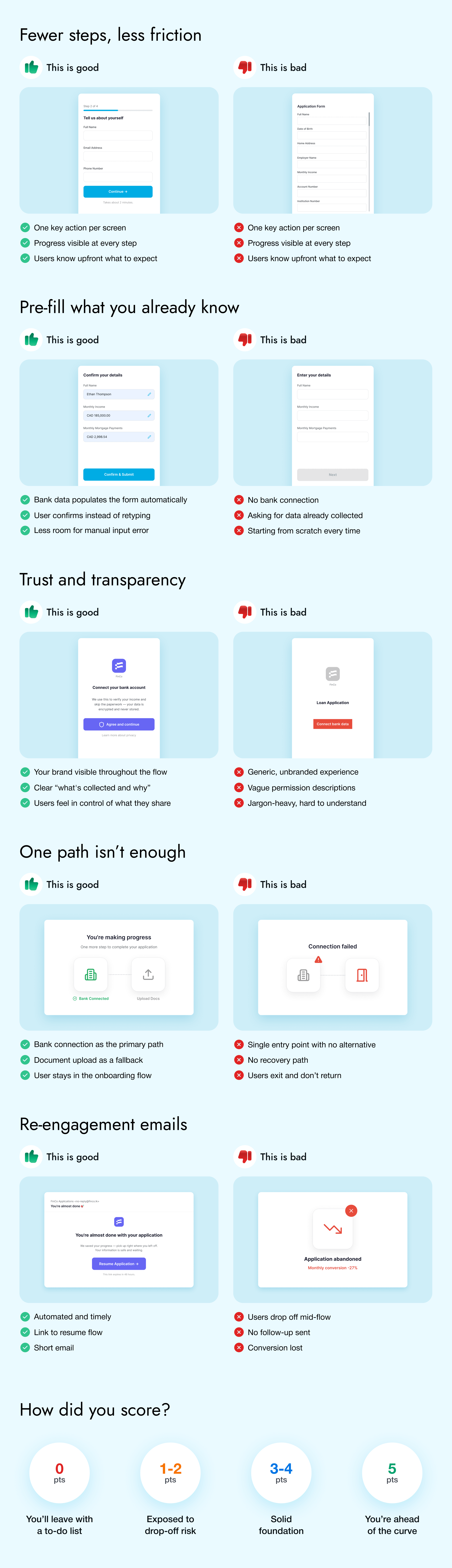

Score your own flow

Here's a quick diagnostic, adapted from the exercise we ran with attendees at our recent webinar. Give yourself a point for each:

- Fewer steps, less friction. Does your flow show users how many steps are involved and where they are in the process? Can they see an estimated time to completion?

- Pre-populated data. If you're using bank connectivity or enrichment data, are you surfacing that to reduce what users have to type — and using discrepancies as fraud signals?

- Trust and transparency. Is your brand visible throughout the flow? Does the user understand at each step what data is being requested and why?

- Flexibility. Can a user who doesn't want to connect their bank account upload a document instead and reach the same outcome? Can they choose the path that fits their comfort level?

- Re-engagement. If a user drops off — because their kid needed them, or they joined a meeting — can they pick up where they left off? Do you have a re-engagement email sequence to bring them back?

Fewer than four out of five is a meaningful gap. And notably, question five is where most teams have the highest headroom: re-engagement and resume functionality are frequently missing from flows that otherwise score well, and they're among the highest-leverage additions a product team can make.

Why is this extra hard in Canada?

The context that shapes all of this is Canada's open banking timeline. The consumer-driven banking framework is still maturing. Most Canadian financial institutions are still accessed via screen scraping, not OAuth APIs, which means connection rates fluctuate when bank interfaces change, and which means Canadian users are newer to the experience of connecting bank accounts as part of a product flow.

That has two practical implications.

First, it raises the bar on the trust and transparency layer. An American fintech can reasonably assume a higher baseline of consumer comfort with open banking. A Canadian company can't, which means the "why are you asking for this?" question needs a better answer in the onboarding flow than it might elsewhere.

Second, it makes document upload not a fallback but a feature. Flinks Upload — the ability to submit a PDF or image of a bank statement — isn't a consolation prize for users who couldn't connect their account. It's the right path for a meaningful share of Canadian users. The best-converting onboarding flows we've seen offer both: connect your bank account, or upload a document, with the user in control of which. Connect and Upload together consistently outperform either path alone.

What you should be able to see

Diagnosing an onboarding problem requires data you may not currently have.

Most companies can see that drop-off happened. They can't see where, why, or who was affected. That's the visibility gap that produces the loop of looking at outcomes and guessing at causes.

Flinks Connect fires events at every step of the bank-connection widget: which institution a user selected, where they stopped, whether they went back and forth. The most sophisticated onboarding flows listen to those events, take action on them (surfacing help at a point of confusion, for example), and use them to build re-engagement sequences that know exactly where to pick up.

Beyond that: knowing when one financial institution underperforms against platform benchmarks lets you route users to Upload as a fallback while the issue gets resolved, rather than losing them entirely. Geographic data tells you where users are connecting and helps teams tailor campaigns by region. These aren't nice-to-haves — they're the difference between guessing at a fix and knowing what to change.

Flinks' client success team produces enhanced drop-off reports that show not just where users are abandoning but what the likely causes are, and what specific changes in the flow have historically improved completion. Those reports are available through your relationship manager and power the one-on-one onboarding reviews we offer to customers.

What the best flows have in common

Two customers worth looking at:

Bree replaced manual document review with real-time bank data via Flinks. The result was a fully automated decisioning flow: customers apply and receive funds in under 10 minutes, with 90%+ bank connection success rate. No manual handoffs.

Wealthsimple embedded Flinks to handle KYC and bank account verification in a single flow. Customers go from sign-up to first investment without paperwork. They offer a manual path, but the Flinks-powered route is positioned clearly as the faster option — and they make the case for it at the point of choice.

What these two have in common isn't a budget or a sophisticated engineering team. It's that they thought deliberately about the process, not just the outcome. They built for the user who's unsure, offered alternatives, and made re-engagement possible when life interrupted the flow.

Onboarding is where acquisition meets activation. Every drop-off is a customer you spent money to acquire but never converted. Getting it wrong doesn't just affect conversion — it affects every downstream metric: engagement, retention, and the likelihood that a customer ever makes you their primary financial relationship.

If you want to understand where your current flow stands, we offer onboarding reviews for existing and prospective Flinks customers. Send us a message, and we can walk through your specific setup.

This post draws on the May 2026 Flinks webinar on financial onboarding, co-hosted with Arber Ago, Enterprise Relationship Manager at Flinks. Watch the full recording below.

.png)