.png)

Access to financial data isn’t the bottleneck anymore, orchestration is.

APIs are becoming more mature, connectivity is widely available, and most teams can retrieve financial data when they need it. Yet onboarding flows continue to break, decisions are made on incomplete signals, and fraud is becoming harder to detect.

What matters now is whether that data actually works inside your workflows across onboarding, verification, and decisioning.

In many cases, this isn’t about new tools or technology. It’s about better leveraging what already exists. At Flinks, companies often come to us with a specific pain point, but uncover opportunities they didn’t initially expect, with impact across the broader financial journey.

Even if you’ve evaluated Flinks before, you might be surprised by how much it has evolved.

Onboarding drives conversion. And it’s where things break

Onboarding isn’t a setup step. It’s a conversion lever.

Users drop off before they ever reach the value of your product when the onboarding experience introduces friction early in the journey. Even strong financial products underperform when the path to get started is not optimized.

The friction usually shows up in a few ways:

- Users are forced into a single way of providing data, rather than flexible options

- Long forms ask for information that could be retrieved automatically

- Document uploads require manual analysis and back-and-forth when data is incomplete

- Trust breaks down when users don’t feel confident sharing sensitive financial information

These aren’t edge cases. They’re common failure points.

Modern financial experiences approach user onboarding differently. They design for flexibility and reduce unnecessary effort across the flow.

This is where Flinks plays a critical role.

Using Flinks Connect, users and merchants can instantly connect their bank accounts and share financial data in seconds. When connectivity isn’t available or preferred, Flinks Upload allows them to submit documents as a fallback without breaking the experience.

That flexibility reduces drop-offs and directly improves conversion and revenue.

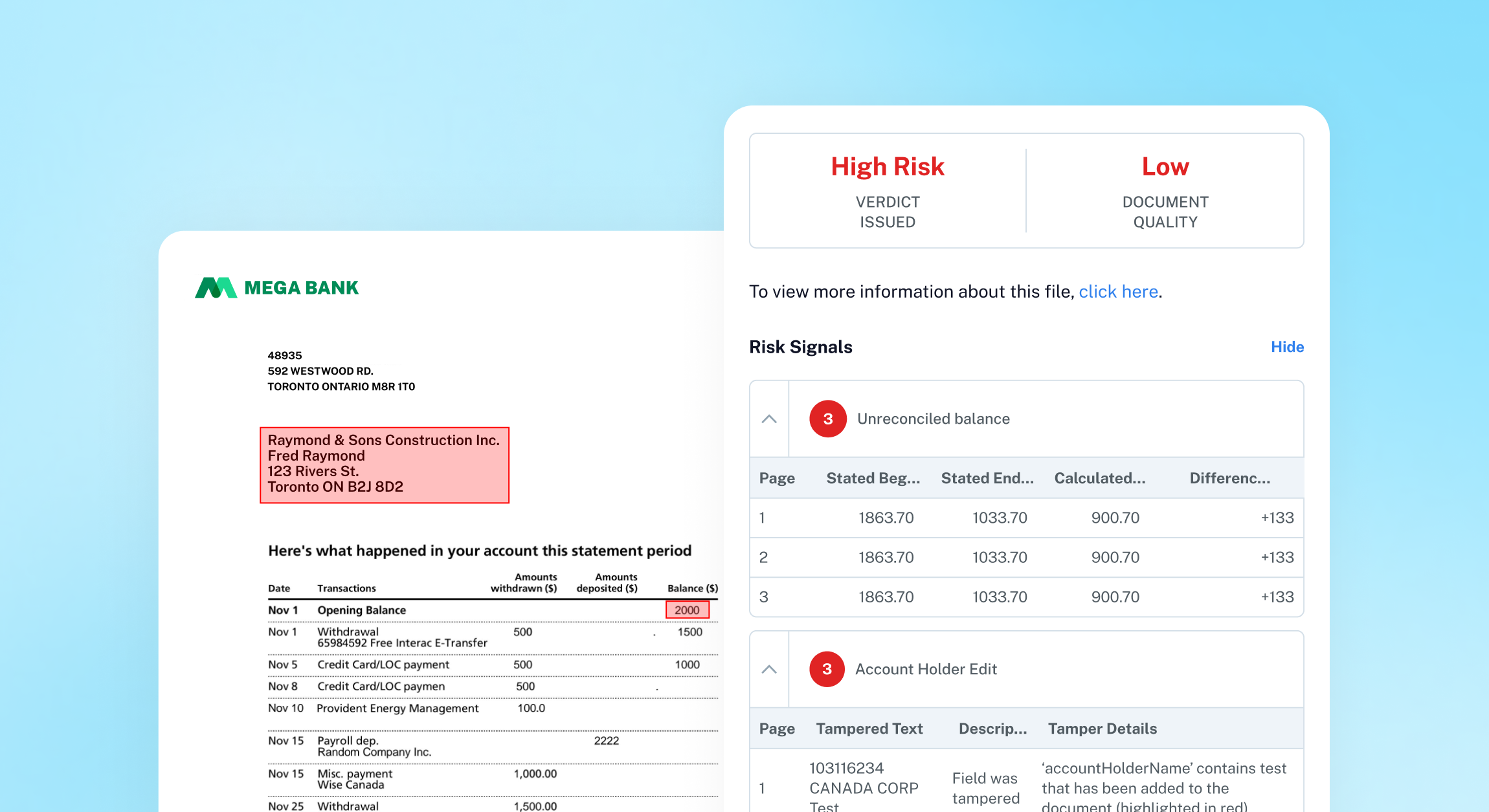

Financial verification is breaking down

Completing onboarding doesn’t solve the next problem: trusting the data.

Traditional income verification methods are losing reliability:

- Credit scores are backward-looking and miss real-time financial behavior

- Documents are increasingly easy to manipulate, especially with AI-assisted fraud

- Self-reported data is inconsistent and difficult to validate

At the same time, financial behavior is becoming more complex. With the rise of the gig economy, income is less predictable, risk is more nuanced, and the signals that matter don’t always appear in static data sources.

That’s why teams are shifting toward verified, enriched transaction data to understand what’s actually happening. Instead of relying on what users report, they analyze real financial activity: cash flow patterns, income signals, spending behavior, and anomalies across accounts.

This is where Flinks Enrich becomes essential.

Flinks Enrich transforms raw transaction data into actionable insights through more than 4,500 enriched attributes. It enables teams to verify income, detect risk signals, and build a clearer picture of financial health.

The result is stronger verification, smarter decisions, and less exposure to risk.

Verification needs to be a continuous layer

Financial verification used to happen at a single point in time. That model no longer works.

Today, verification needs to support the entire workflow — from onboarding to decisioning to money movement.

When financial data is verified early and continuously, everything downstream improves. Onboarding becomes smoother, decisions become more reliable, and transactions are more likely to succeed.

Flinks enables this through instant bank verification (IBV) capabilities embedded across its products. That same foundation extends into payments with Flinks Pay, where money movement is built on verified financial data, helping reduce failed transactions.

Where teams are evolving their approach

What’s changing isn’t just technology. It’s how teams think about financial workflows — and how they fully leverage partners like Flinks.

Across industries, a few consistent patterns are emerging:

From connectivity to financial data foundation

Many organizations initially work with Flinks to connect bank accounts. Over time, that connectivity becomes the foundation for onboarding, verification, and data-driven workflows across the business.

From document collection to document intelligence

Collecting documents digitally is table stakes. With Flinks Upload, they become structured, analyzable data that can be verified to prevent document fraud, power smarter decisions, and reduce manual reviews.

From verification to decisioning

Verification is no longer just about confirming identity or account ownership. With Flinks Enrich, financial data becomes a core input into underwriting, risk assessment, and financial analysis.

From payments to verified money movement

Payments are often treated as a separate workflow. With built-in verification through Flinks Pay, account verification and money movement are connected, reducing failures and improving transaction success.

This is where many teams start to unlock the full value of Flinks as the infrastructure that supports multiple workflows.

Where this shows up beyond core workflows

Flinks has historically been associated with lending use cases. That’s where many companies first encountered us. But our platform has expanded well beyond that, and now supports a broader set of workflows across industries:

Tenant screening

Platforms can verify income and assess financial stability using real transaction data, reducing reliance on credit scores and pay stubs while improving fraud detection and decision confidence.

Transaction reconciliation

Accounting and financial platforms use structured and normalized transaction data from Flinks Enrich to automate reconciliation, improve accuracy, and reduce manual effort across fragmented financial inputs.

Merchant onboarding

Flinks supports faster and more reliable business onboarding by combining bank connectivity, document processing, and financial data validation to streamline KYB workflows and reduce friction.

Different use cases, but the same underlying advantage: financial data that is reliable, structured, and ready to use.

A final thought

When onboarding, verification, and decisioning are designed as separate steps, performance breaks down.

When they are orchestrated as a single system, the impact is clear: higher conversion, faster decisions, stronger risk control, and more reliable transactions.

If you’re exploring how to better connect these pieces, it may be worth revisiting what’s possible with Flinks – just reach out to our team to continue the conversation.

.png)